Wicheeda Project

100% OWNED

Strategically positioned

80 km from Prince George and accessible from a major forestry service road, which connects to Highway 97.

100%

owned

11,800-hectare Wicheeda deposit has power transmission lines, a gas

pipeline and a major rail line nearby.

Prince George,

British Columbia is a mining centre with a skilled workforce.

Port of

Prince Rupert

is 500km to the west and accessible by rail and road.

2025 Mineral Resource

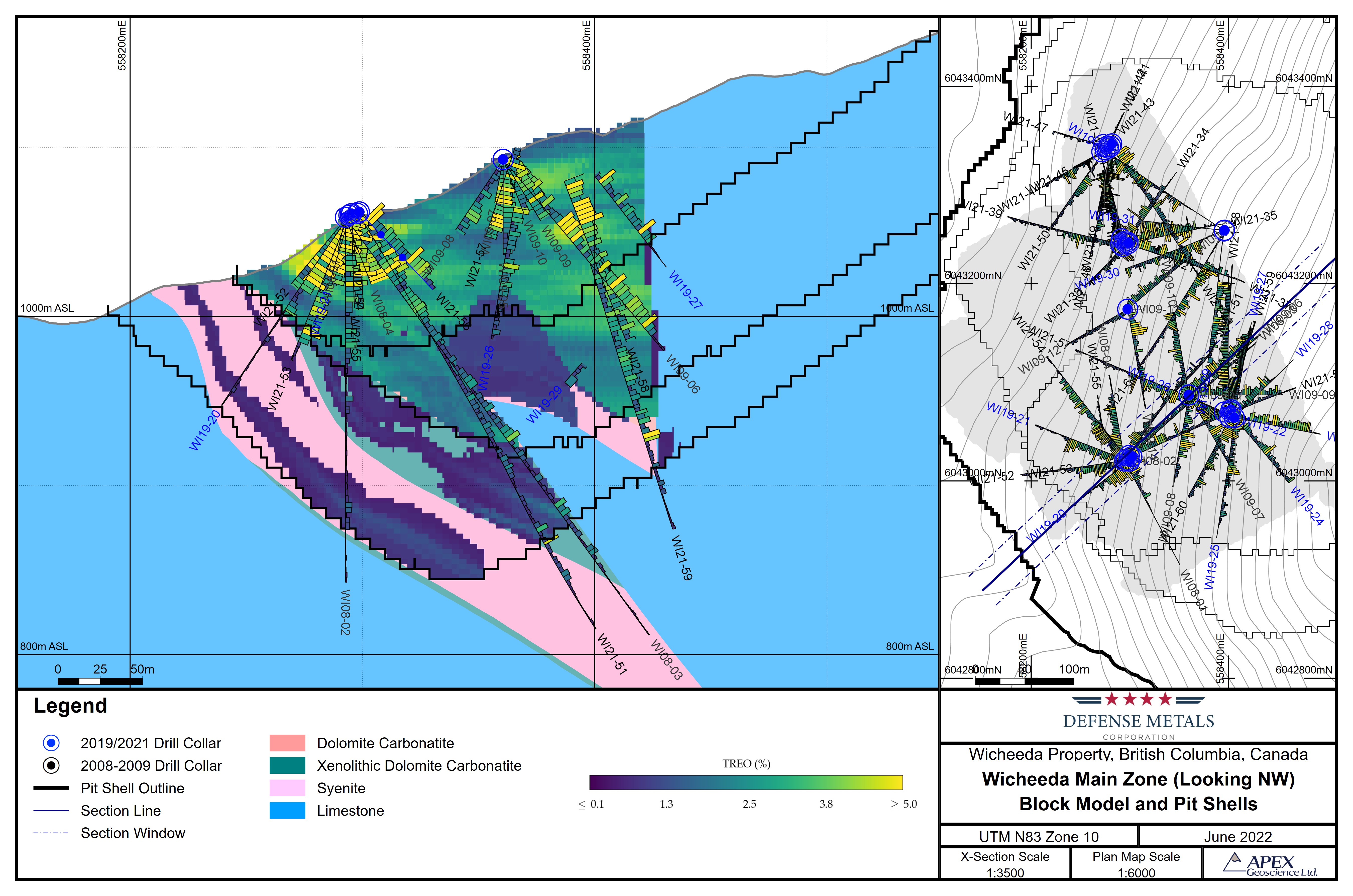

The Wicheeda REE deposit is a southeast-trending, north to northeast dipping syenite-carbonatite intrusive complex having dimensions of approximately 450 m north-south by 250 m east-west which intrudes a mixed sedimentary host rock package (limestone). Relatively high REE grade dolomite-carbonatite rocks, which outcrop at surface, and form the main body of REE mineralization are surrounded by an envelope of intermediate REE grade hybrid xenolithic-carbonatite rocks that intrude lower REE grade syenite.

The Mineral Resource estimate for the Wicheeda Rare Earth Element Deposit has been prepared for Defense Metals as part of the 2025 Pre-Feasibility Study (PFS). This Mineral Resource estimate has been prepared in accordance with the CIM Definition Standards adopted May 2014.

The Mineral Resources stated below are constrained within an optimized pit shell to satisfy Reasonable Prospects of Eventual Economic Extraction (RPEEE) requirements. The Mineral Resources include 29.2 Mt of Measured + Indicated resource at an average grade of 2.27% TREO and 5.5 Mt of Inferred resource at an average grade of 1.42% TREO. No mining dilution has been incorporated into the Mineral Resources stated below. The Mineral Resources are stated inclusive of Mineral Reserves.

A summary of the surface mineable Mineral Resources by rock type and Resource classification is shown below.

Notes for Resource Table:

-

CIM (2014) definitions were followed for Mineral Resources.

-

The Qualified Person for the MRE is Doug Reid, P.Eng., EGBC (23347), an SRK employee.

-

The effective date of the Mineral Resource is February 7, 2025

-

Dollar values herein stated are United States Dollars (US$)

-

Mineral Resources are reported assuming the prices listed below (a 15% uplift was applied to the Reserve prices):

• NdPr Oxide 132.70 $/kg REO

• Tb4O7 1567.26 $/kg REO

• Dy2O3 508.85 $/kg REO -

Mineral Resources are defined within a pit shell derived from the optimization software, GEOVIA Whittle™

-

Cut-off grade is based on the value factors generated in each block. The revenue and related costs vary based on the

composition of different elements in each block. Value of a block is the revenue generated in that block minus the related

processing and G&A operating costs. -

The base mining costs are assumed to be $4.50/t. The mining costs vary based by the bench and depth of the pit. The

average mining costs for the life of mine is calculated to be $4.74/t mined. -

Processing costs consist of flotation plant cost at the mine site and a hydrometallurgical/solvent extraction

(hydrometallurgical) plant that is off the mine property. The operating cost of the flotation plant is $27.60/t milled and the

hydrometallurgical plant operating cost is $1,164.4/t of concentrate treated. -

General and administration costs of the mine site is $3.67/t for ore milled.

-

Tailings management and storage cost is $6.55/t of ore.

-

Off-site cost (transportation) is $87.76/t of precipitate products produced.

-

Processing recovery is calculated using the following formula:

• Flotation recovery for TREO = -11.183*TREO^2 + 67.831*TREO - 20.421940%. For ore above 3% TREO

the flotation recovery is set to 82.4%. For grade less than 0.32% TREO the flotation recovery is set to 0.0%.

• Flotation recovery for TREO then is multiplied by 0.995, 0.996, 0.734, 0.636 for Pr, Nd, Tb, Dy respectively

to calculate the respective flotation recovery for each element.

• Hydrometallurgical recovery for Pr, Nd, Tb, Dy are 0.932, 0.935, 0.802, 0.734 respectively -

A 95% payability has been applied to the final hydrometallurgical product.

-

Bulk density is assigned by lithology.

-

No mining dilution has been applied.

-

Mineral Resources are reported inclusive of those Mineral Resources converted to Mineral Reserves.

-

Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability.

-

Figures are rounded to the appropriate level of precision for the reporting of mineral Resources. Due to rounding, some

columns or rows may not sum as shown. -

The TREO grade encompasses 15 rare earth elements present in the deposit.

-

The estimate of Mineral Resources may be materially affected by environmental, permitting, legal, title, taxation,

sociopolitical, marketing, or other relevant issues.

Property Geology

REE-enriched carbonatites of the Wicheeda Deposit are part of an elongate, northwest trending intrusive carbonatite-syenite sill complex. The carbonatite is intruded into syenite, mafic dikes, limestone, and calcareous sedimentary wall rocks. The Wicheeda REE Deposit has dimensions of approximately 400 m north-south by 100-250 m east-west.

Diamond drilling data supports the interpretation of a moderately north-northeast dipping, shallowly north plunging, layered sill complex having syenite at its base. It is overlain by hybrid matrix to clast-supported limestone or mafic intrusive xenolithic carbonatite (fenite), as well as significantly REE-bearing dolomite-carbonatite rocks, which form the main body of the Wicheeda REE Deposit outcropping at surface. This layered sill complex occurs within an unmineralized limestone waste rock.

Property Location

Strategically positioned along a major forestry service road, which connects to BC Highway 97.

A major hydroelectric power line, a major gas pipeline, and a Canadian National Railway line are available nearby.

Prince George, British Columbia, a mining centre with a skilled workforce, is 80km to the southwest.

Port of Prince Rupert is 500km to the west and accessible by rail and road.

Wicheeda Long Section BM & Pit 2023

2023 Resource Main Zone Section